Routing Number: 263178070 *APR = Annual Percentage Rate.

©2025 Eglin Federal Credit Union. Eglin Federal Credit Union is Federally Insured by NCUA. Equal Housing Lender (NMLS 440642). Equal Opportunity Employer. Information submitted to Eglin FCU via email is not encrypted and may not be secure. Links to other sites are provided as a convenience to our visitors. The Credit Union is not responsible for the availability, content, or privacy practices of any linked site. Images used for representational purposes only; do not imply government endorsement. If you experience any problems accessing our website or using online services, please call 800.367.6159 during our normal business hours (Monday-Friday 9am-5pm CST, excluding federal holidays).

When you receive a collateral loan from Eglin FCU you'll need to agree to maintain adequate insurance coverage.

|

Alfa Romeo Maserati Pensacola |

|

Allen Turner Chevrolet |

|

Allen Turner Genesis |

|

Allen Turner Hyundai |

|

Anderson Subaru |

|

Audi Pensacola |

|

Bay Chrysler Dodge Jeep RAM |

|

Bay Lincoln |

|

Bay Mitsubishi |

|

BMW of Fort Walton Beach |

|

Buick GMC Fort Walton Beach |

|

Centennial Imports |

|

Chrysler Dodge Jeep Ram Crestview |

|

Chrysler Dodge Jeep Ram Fort Walton Beach |

|

David Scott Lee Buick GMC |

|

David Scott Lee Ft. Walton Beach |

|

First Choice Automotive |

|

Ford Crestview |

|

Ft. Walton Mitsubishi |

|

FWB Auto Brokers |

|

Gary Smith Ford |

|

Gary Smith Honda |

|

Hampton Hyundai Genesis Imports |

|

Hill Kelly Dodge |

|

Kia Fort Walton Beach |

|

Lee Nissan |

|

Mazda of Fort Walton Beach |

|

McKenzie Buick GMC |

|

Mercedes-Benz of Fort Walton Beach (ZT Motors) |

|

Orr Porsche of Destin |

|

Pensacola Honda |

|

Pete Moore Chevrolet |

|

Pete Moore Imports |

|

Preston Hood Chevrolet |

|

Sandy Sansing BMW Mini Cooper |

|

Sandy Sansing Chevrolet |

|

Sandy Sansing Chrysler Dodge Jeep Ram |

|

Sandy Sansing Mazda |

|

Sandy Sansing Milton Chevrolet LLC |

|

Sandy Sansing Nissan Inc. |

|

Step One Automotive BGC PN LLC |

|

Subaru Fort Walton Beach |

|

Tim Smith Acura |

|

Toyota of Fort Walton Beach |

|

Volkswagen Fort Walton Beach |

|

World Ford Pensacola |

Questions? Call 850.862.0111 option 2 or email Consumer Loans via secure email.

| Vehicle type | Term | APR* (as low as) |

| New or Used Up to 15 Years Old | 66 Months | 5.99% |

| New or Used Up to 10 Years Old | 74 Months | 6.49% |

| New or Used Up to 10 Years Old ($20k +) | 84 Months | 7.49% |

* APR = Annual Percentage Rate. There is a range of rates for each loan type. The rate received will be determined by an evaluation of the applicant's credit. The above rates are current as of Monday, June 30, 2025 and are subject to change

A New Auto is one that has never been titled. A Used Auto is one that has previously been titled.

Questions? Call 850.862.0111 option 2 or email Consumer Loans via secure email.

| Loan value | Loan term | APR*(as low as) |

| Up to $10,000 | 60 Months | 6.75% |

| Up to $25,000 | 120 Months | 7.75% |

| Up to $50,000 | 144 Months | 8.00% |

| Over $50,000 | 180 Months | 8.00% |

| Loan value | Loan term | APR*(as low as) |

| Up to $10,000 | 60 Months | 7.75% |

| Up to $25,000 | 120 Months | 8.75% |

| Up to $50,000 | 144 Months | 9.00% |

| Over $50,000 | 180 Months | 9.00% |

Questions? Call 850.862.0111 option 2 or email Consumer Loans via secure email.

| Loan value | Loan term | APR*(as low as) |

| Up to $10,000 | 60 Months | 6.75% |

| Over $10,000 | 120 Months | 7.75% |

| Over $25,000 | 144 Months | 8.00% |

| Over $50,000 | 180 Months | 8.00% |

| LOAN VALUE | LOAN TERM | APR*(as low as) |

| Up to $10,000 | 60 Months | 7.75% |

| Over $10,000 | 120 Months | 8.75% |

| Over $25,000 | 144 Months | 9.00% |

| Over $50,000 | 180 Months | 9.00% |

| Loan value | Loan term | APR*(as low as) |

| Up to $10,000 | 60 Months | 6.00% |

| Over $10,000 | 72 Months | 7.75% |

| Over $20,000 | 84 Months | 8.25% |

Questions? Call 850.862.0111 option 2 or email Consumer Loans via secure email.

| Loan value | Loan term | APR*(as low as) |

| Up to $10,0001 | 48 Months | 7.00% |

| Over $10,0002 | 60 Months | 7.00% |

| Loan term (up to) | APR*(as low as) |

| 60 Months | 6.00% |

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| LOAN TERM | APR* | ORIGINATION FEE | POINTS |

| 30 year | 6.500% | 0% | 0 |

| 20 year | 5.875% | 0% | 0 |

| 15 year | 5.500% | 0% | 0 |

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| LOAN TERM | APR* | ORIGINATION FEE | POINTS |

| 30 year | 6.500% | 0% | 0 |

| 20 year | 5.875% | 0% | 0 |

| 15 year | 5.500% | 0% | 0 |

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| LOAN TERM | APR* | ORIGINATION FEE | POINTS |

| 30 year | 6.500% | 0% | 0 |

| 20 year | 5.875% | 0% | 0 |

| 15 year | 5.500% | 0% | 0 |

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| INTEREST RATE | MAXIMUM COMBINED LTV** (TLTV) |

| 6.50% APR* | 80% |

| Interest Rate | Minimum Advance | Closing Costs |

| 7.50% APR* | $5,000** | NONE** |

*APR = Annual Percentage Rate. The APR is variable and is based on the Wall Street Journal U.S. Prime Rate which was 7.50% as of 12/19/2024. The maximum APR will not exceed 18% and the minimum APR will not be reduced below 3% at any time during the term of the plan.

**If you chose to participate in our current Home Equity Line-of-Credit Plan Promotion, Eglin FCU will pay closing costs for bona-fide third party fees (except for an appraisal or costs associated with a purchase/deed) up to $3,000. Member agrees to reimburse Eglin Federal Credit Union for the bona-fide third party fees paid if the Plan is closed within 36-months of the loan origination date. A minimum advance of $5,000 will be required at closing with this promotion.

Maximum Loan Amounts & Restrictions - Home Equity Line of Credit

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| MAX TERM | APR* |

| 5 years | 8.50% |

| 10 years | 9.00% |

Questions?

Contact our Mortgage Services team today at 850.862.0111 x.3737 or via secure email

| MAX TERM | APR* |

|---|---|

| 9 months | 5.50% |

| LOAN TERM | APR* as low as | MAX LOAN AMOUNT |

| 42 Months | 8.90% | $20,000 |

| LOAN TERM | APR* as low as | MAX LOAN AMOUNT |

| ------ | 8.90% | $20,000 |

| REPAYMENT PERIOD | APR* | MAX LOAN AMOUNT |

| 120 days | 16.9% | $500 |

| REPAYMENT PERIOD | APR* as low as | MAX LOAN AMOUNT |

| 42 Months | 13.90% | $3000 |

| REPAYMENT PERIOD | APR* as low as | MAX LOAN AMOUNT |

| 42 Months | 5.00% | $2000 |

| LOAN TYPE | MAX LOAN AMOUNT | REPAYMENT PERIOD | APR* |

| Share Loan Pledging S1 or S4 | Available balance in account pledged | 84 months | 2.00% |

| Share Loan Pledging S7 | Available balance in account pledged | 84 months | 2.5% |

| Share Certificate Loan | Available balance of Share Certificate | Paid at maturity of Share Certificate | 3% above Share Certificate Rate |

| PREMIUM CHECKING | DIVIDEND RATE | APY* |

| A $500 minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.05% | 0.05% |

| REGULAR SHARE SAVINGS | DIVIDEND RATE | APY* |

| A $50 daily minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.35% | 0.35% |

| FL UNIFORM TRANSFER TO MINORS SAVINGS | DIVIDEND RATE | APY* |

| A $50 daily minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.35% | 0.35% |

| CHRISTMAS CLUB SAVINGS | DIVIDEND RATE | APY* |

| A $50 daily minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.35% | 0.35% |

| VIP SAVINGS | DIVIDEND RATE | APY* |

| A $50 daily minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.35% | 0.35% |

The Current APY and Dividend Rates shown are the current weekly rates in effect from 6/27/2025 - 7/3/2025. The Previous APY and Dividend Rate stated are accurate as of the last dividend declaration date, which is the last day of the previous month. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends.

|

Money Market Balance |

Current Dividend Rate |

Current APY* |

Previous Dividend Rate |

Previous APY* |

| $.00 to 2,499.99 | 0.05% | 0.05% | 0.05% | 0.05% |

| $2,500.00 to 9,999.99 | 0.95% | 0.95% | 0.95% | 0.95% |

| $10,000.00 to 24,999.99 | 1.00% | 1.01% | 1.00% | 1.01% |

| $25,000.00 to 49,999.99 | 1.05% | 1.06% | 1.05% | 1.06% |

| $50,000.00 & up | 1.10% | 1.11% | 1.10% | 1.11% |

| COVERDELL EDUCATION SAVINGS | DIVIDEND RATE | APY* |

| A $50 daily minimum balance is required to earn dividends. The APY stated is accurate as of the last dividend declaration date, which is the last day of the previous quarter. Dividend rate and APY are variable and subject to change after the account is opened. If you close your account before dividends are paid you will not receive the accrued dividends. | 0.35% | 0.35% |

A $50 daily minimum balance is required to earn dividends. All Current APY and Dividend Rates shown are the current weekly rates in effect on 6/27/2025. Dividend rate and APY are variable and subject to change after the account is opened. The Previous APY and Dividend Rates stated are accurate as of the last dividend declaration date, which is the last day of the previous quarter.

| Account Description | Current Dividend Rate | Current APY* | Previous Dividend Rate | Previous APY* |

| Traditional IRA | 3.85% | 3.92% | 3.95% | 4.03% |

A $50 daily minimum balance is required to earn dividends. All Current APY and Dividend Rates shown are the current weekly rates in effect on 6/27/2025. Dividend rate and APY are variable and subject to change after the account is opened. The Previous APY and Dividend Rates stated are accurate as of the last dividend declaration date, which is the last day of the previous quarter.

| Account Description | Current Dividend Rate | Current APY* | Previous Dividend Rate | Previous APY* |

| Roth IRA | 3.85% | 3.92% | 3.95% | 4.03% |

A $2500.00 minimum deposit required. There is a penalty for early withdrawal.

Rates listed are current from 6/27/2025 - 7/3/2025.| CERTIFICATE TYPE | DIVIDEND RATE | APY* |

| 31 Days / 1 month Certificate | 3.50% | 3.56% |

| 92 days / 3 month Certificate | 3.50% | 3.56% |

| 182 days / 6 month Certificate | 3.80% | 3.87% |

| 365 days / 12 month Certificate | 3.90% | 3.97% |

| 548 days / 18 month Certificate | 3.95% | 4.02% |

| 730 days / 24 month Certificate | 3.85% | 3.92% |

| 1095 days / 36 month Certificate | 3.75% | 3.82% |

| 1460 days / 48 month Certificate | 3.70% | 3.76% |

| 1825 days / 60 month Certificate | 3.65% | 3.71% |

| Annual Percentage Rate (APR) for Purchases, Balance Transfers, and Cash Advances | as low as 7.9% up to 14.9% The APR is determined at account opening and is based on the borrower's credit score. |

| Penalty APR | None |

| Paying Interest | Your due date is at least 24 days after the close of each billing cycle. We will not charge you interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on cash advances and balance transfers on the transaction date |

| Minimum Interest Charge | None |

| For Credit Card Tips from the Consumer Financial Protection Bureau | To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at http://www.consumerfinance.gov/learnmore |

| Annual Fee | None |

| Transaction Fees | |

| Balance Transfer | None |

| Cash Advance | None |

| International Transaction | None |

| Penalty Fees | |

| Late Payment | $20 or the amount of the required minimum payment, whichever is less, if you are 12 or more days late in making a payment. |

| Over-the-Credit-Limit | None |

| Returned Payment | Up to $28.00 |

| Annual Percentage Rate (APR) for Purchases, Balance Transfers, and Cash Advances | as low as 8.9% up to 15.9% The APR is determined at account opening and is based on the borrower's credit score. |

| Penalty APR | None |

| Paying Interest | Your due date is at least 24 days after the close of each billing cycle. We will not charge you interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on cash advances and balance transfers on the transaction date |

| Minimum Interest Charge | None |

| For Credit Card Tips from the Consumer Financial Protection Bureau | To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at http://www.consumerfinance.gov/learnmore |

| Annual Fee | None |

| Transaction Fees | |

| Balance Transfer | None |

| Cash Advance | None |

| International Transaction | None |

| Penalty Fees | |

| Late Payment | $20 or the amount of the required minimum payment, whichever is less, if you are 12 or more days late in making a payment. |

| Over-the-Credit-Limit | None |

| Returned Payment | Up to $28.00 |

When you received your loan you agreed to maintain adequate insurance coverage. If your insurance information has changed or you receive a letter stating we do not have proper documentation, you should provide us with a copy of your insurance declarations page (not your insurance card). The declarations page must show the following information:

Eglin Federal Credit Union uses small text files called cookies to collect anonymous Web site traffic data. This information helps improve our Web services. Our cookies do not collect or store any personally identifiable information.

To help fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens or signs on an account.

When you open an account, we will ask you for your name, physical address, date of birth and other information that will allow us to identify you.

Please refer to the following guidelines for providing your account number:

In compliance with The Secure and Fair Enforcement for Mortgage Licensing Act, also known as the SAFE Act, we provide a list of Eglin FCU's registered mortgage loan originators and their Nationwide Mortgage Licensing System (NMLS) number on our website. The SAFE Act was passed to ensure the integrity of the Mortgage Lending system by establishing a set of standards that specific mortgage professionals must meet in order to work in the mortgage industry.

| Eglin FCU Mortgage Professional | NMLS ID |

| Aimee N Wilson | 2536346 |

| Ann Creager | 1561554 |

| Ashley Lynn Ellis | 2701133 |

| Ashley Hall | 1011145 |

| Brian Mark Franks | 1296056 |

| Carole Stanley | 1482257 |

| Carrie Ann Calcutt | 2064000 |

| Christina Walker | 1714720 |

| Christy Milian | 490970 |

| Cynthia Bower | 2064007 |

| Elisabeth Diana Good | 2664398 |

| Jaime Lynn O'Callaghan | 2697800 |

| Jennifer Leigh Wyatt | 2329051 |

| Jesus Abad Morales Ramos | 2675473 |

| John Pellerin | 1011113 |

| John Francis Stackpoole | 2398303 |

| Judith Anne Turner | 2311448 |

| Kayla Michelle Smith | 2177769 |

| Lilly B. Edra | 2041564 |

| Lisa Diane Freeland | 2367009 |

| Mary Ann Geoghagan | 2329070 |

| Michelle (Beth) Bethanne Meverden | 2460346 |

| Michele (Shellie) Marie Fite | 798447 |

| Mindy Danielle Dumas | 2496680 |

| NormaJean Enlow | 1212774 |

| Rebecca Jean Snow | 2484799 |

| Ruby Tincher | 1212771 |

| Samara Genine Simeone | 2672002 |

| Sheeny Marquez Satulan | 2237420 |

| Susan Castillo Dombrigues | 490967 |

| Tatyana Galenkova | 2063947 |

| Teally Goodson Gorey | 2421096 |

| Tiffany Michelle Cadogan | 1867034 |

| Yolanda Harrison | 805809 |

| Zena Payne | 490969 |

| Eglin FCU | 440642 |

eStatements provide online access to your account statements instead of by mail. Besides being an excellent way to help our environment, going paperless is also a fast, convenient and safe way to view your monthly statement. This service is free to all Eglin FCU members and can be cancelled at any time. To receive eStatements, Online Banking is required.

Set up eStatements today by logging in and selecting 'eStatements' under the 'eServices' tab in the main navigation.

We recommend that members with Online Banking log in to make these changes in the "Contact Information" section under the "My Profile" tab.

Please note: For the safety and security of our members, some services may be limited for up to 30 days after an address change. Print the Change of Contact Information form to submit it in person at an Eglin FCU branch.

Complete the skip-a-pay form to agree to the terms* and request your preference to skip your next loan payment on your Eglin FCU loan product. Please note: It may take up to 2 business days to process your request. If submitted via DocuSign, you will receive a confirmation email when your request has been processed. If you have questions or need additional assistance, please call 850.862.0111 or 800.367.6159.

*Subject to approval. Your account must be in good standing. This offer is subject to a $20 processing fee for each loan payment skipped. Only one skip allowed per loan per calendar year. This offer excludes Mastercard®, S.A.F.E. Loans, Share Certificate Loans, Mortgage Loans, and Mobile Home Loans. Loan must be at least one year old. Skipping a payment will extend the repayment period on the loan and interest continues to accrue during the skip period. Except as expressly amended by this agreement the terms of the original loan agreement remain in full force and effect. Annual Percentage Rate and scheduled payment do not change. GAP protection coverage will be reduced if you skip or miss more than 2 monthly payments over the life of the loan.

| Holiday | Date |

| Name | Title |

| Cathie Staton | President/Chief Executive Officer |

| Gina Denny | SVP/Chief Human Resources Officer |

| Tim Farnsworth | SVP/Chief Technology Officer |

| C. Grant | SVP/Chief Financial Officer |

| Rocky Magee | SVP/Chief Information Officer |

| Kim Nauta | SVP/Chief Operations Officer |

| Dawn Oravetz | SVP/Chief Payments Officer |

| Jon Heidt | SVP Risk Management |

| Neko Stubblefield | SVP Membership/Community Development |

| Joe Baldwin | VP Investments |

| Laura Coale | VP Marketing/PR |

| Ashley Hall | VP Mortgage Services |

| David Lancaster | VP Lending |

| Bron Ringstad | VP Branch Operations |

| Name | Title |

| Daniel McInnis | Chair |

| William S. Rone | Vice Chair |

| James Pitts | Secretary/Treasurer |

| Richard Adams | Director |

| Robert Harlan | Director |

| Barbara Patty | Director |

| J. Russ Corbitt | Director |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fort Walton Beach, Fla. (July 28, 2022) - Eglin Federal Credit Union is pleased to announce Procurement Specialist Quentin Youngblood has been selected as the 5-Star Performer of the 2nd Quarter of 2022. Quentin has been employed with the Credit Union since January of 2012 and currently resides in Fort Walton Beach.

President/CEO Jerry Williams said, "Quentin displays exemplary leadership and dedication to members and fellow Credit Union employees. He has a wonderful, cooperative attitude and is an excellent team player."

Manager Kathey Mitchell added, "Quentin does a great job procuring all supplies and furniture for EFCU. He responds to department requests quickly and accurately and ensures our stockroom stays supplied with the items we need. Quentin often takes on additional responsibilities when he sees that something needs to be done."

The 5-Star Performer Award is a quarterly employee recognition program. The nominator provides a written submission describing how the employee exudes EFCU's Five-Star Values: Respectful, Trustworthy, Dedicated, Proactive and Engaged.

"I appreciate the support and recognition from the people I have the pleasure of working with on a daily basis," said Quentin. "I enjoy working at Eglin Federal Credit Union and am happy to contribute to the success of the organization."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Oct. 29, 2021) - Eglin Federal Credit Union is pleased to announce Destin Member Services Counselor Tracy Goodman has been selected as the 5-Star Performer of the 3rd Quarter. Tracy has been with the Credit Union for seven years.

Destin Branch Manager Susan Arnold said at the award presentation, "Members flock to Tracy because she is knowledgeable, trustworthy, courteous and gracious. Tracy is known for her strong work ethic, leadership qualities, and humble attitude. She is always looking for opportunities to expand her knowledge and is committed to her coworkers and the members she serves. Tracy is a shining star, and very worthy of this recognition."

The 5-Star Performer Award is a quarterly employee recognition program. The nominator provides a written submission describing how the employee exudes EFCU's Five Star Values: Respectful, Trustworthy, Dedicated, Proactive and Engaged.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Oct. 29, 2021) - Eglin Federal Credit Union is pleased to announce Laura Coale has been named the VP of Marketing and Public Relations. Coale brings more than 20 years of communications experience in private and public organizations to the Credit Union. In this role, Coale will be responsible for effectively executing integrated marketing initiatives to meet the mission of EFCU.

"We are very happy Laura joined Eglin Federal Credit Union as the new VP of Marketing and Public Relations," said President and CEO Jerry Williams. "Her experience in branding, change communication and creating award-winning marketing and public relations campaigns will greatly benefit the Credit Union's members and the community."

Coale earned her master's degree in journalism and mass communication with a public relations concentration from Kent State University while she was working as the media relations director for Denver International Airport. She earned her bachelor's degree in communication with minors in business management and decision sciences from Miami University in Ohio. She also earned a certified change practitioner certificate from Prosci.

Most recently, Coale worked as the communications director for the Escambia County Board of County Commissioners. During this time, Coale was recognized for assisting the US Attorney's Office and FBI on the NAS Pensacola Terrorist Attack. She also led the team to win the 3CMA Silver Circle Award for a digital interactive COVID-19 public relations campaign, and she led the public information efforts during Hurricane Sally.

"Eglin Federal Credit Union is recognized as a leader in our community, and I am very proud to join this extraordinary team," said Coale. "I'm looking forward to sharing stories about the incredible work employees do in the community and the benefits of the products and services available to members. Eglin Federal Credit Union has a long and rich history serving its members and the community, and I'm thrilled to be able to use my strategic communications experience to help the community in which I live."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

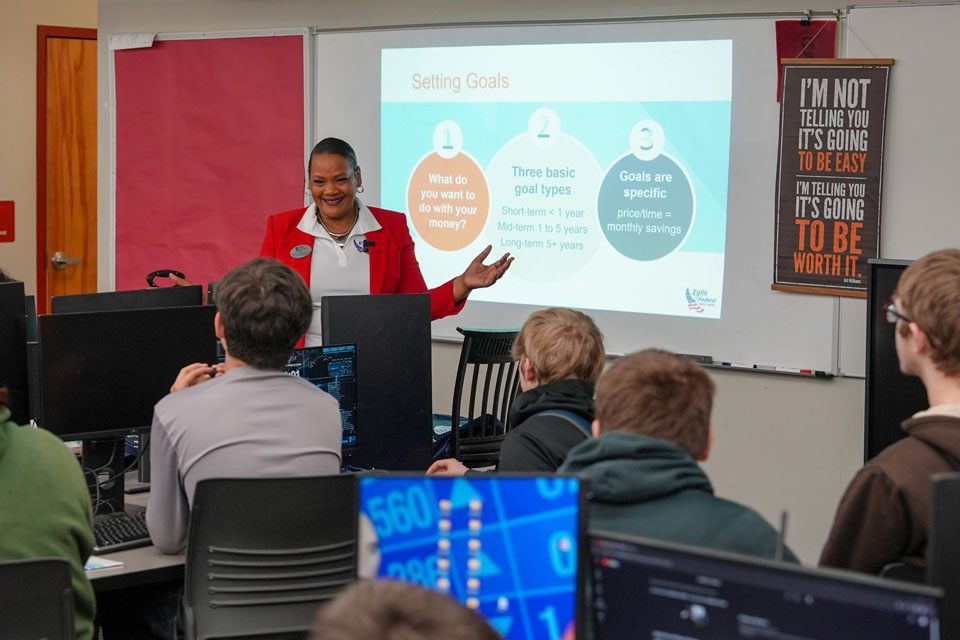

Fort Walton Beach, Fla. (Nov. 12, 2021) - Eglin Federal Credit Union partnered with the Boys and Girls Club of the Emerald Coast (BGCEC) and Hey Gym Friend to conduct a Financial Fitness Bootcamp for approximately 100 youth on Friday, Nov. 5 at Riverside Elementary School in Crestview.

"The kids loved every minute of the Finance and Fitness Bootcamp and can't wait until the next session," said John Bryant, BGCEC campus director, Riverside Elementary. "We are grateful to EFCU for investing their time in our kids and the community."

EFCU VP of Membership and Community Development Neko Stubblefield and Financial Education Specialist Courtney Dollson taught youth about financial wellness with lessons centered on ways to earn, save, spend and donate money. After Courtney and Neko facilitated financial fitness, the youth joined Tonnisha Deonn from Hey Gym Friend for a physical fitness workout. Participants also had a chance to win one of four $25 cash drawings from EFCU.

"We joined forces with the Boys and Girls Club in Crestview to talk about the essentials of finances, savings, donating and giving back to the community," said Neko Stubblefield. "We rounded it out with a fitness bootcamp to have fun. It's our way of giving back to the community by talking about those things that are important for future financial health. It's a great opportunity to start at this level to build healthy financial behaviors that will last a lifetime."

About the Boys & Girls Club of the Emerald Coast

Boys & Girls Clubs programs have taken Members from the Clubhouse to the White House; from the games room to the corporate boardroom; from the high school football field to the NFL; from a band room to Carnegie Hall. In every community, young people are left to find their own recreation and companionship in the streets. An increasing number of children are at home with no adult care or supervision. Young people need to know that someone cares about them.

Boys & Girls Clubs of the Emerald Coast offer that and more. Club programs and services promote and enhance the development of boys and girls by instilling a sense of competence, usefulness, belonging and influence. Boys & Girls Clubs of the Emerald Coast is a safe place to learn and grow - all while having fun. These Clubs are the place where great futures are started each and every day. Learn more at emeraldcoastbgc.org.

About Hey Gym Friend

Hey Gym Friend Founder Tonnisha Deonn created the HGF community after losing 150 pounds. Tonnisha is a certified trainer/nutrition specialist. She envisioned a positive physical environment where self-love and growing socially meet. She made it her mission to make health and fitness fun and stress-free. Hey Gym Friend is a no judgment zone. Positivity is the only requirement!

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Nov. 16, 2021) - Eglin Federal Credit Union is pleased to recognize Chief Strategy Officer Cathie Staton for her 35 years of service with Eglin Federal Credit Union. As chief strategy officer Cathie manages strategic planning, marketing and public relations, membership and community development, risk management and compliance.

Cathie began her career at Eglin Federal Credit Union on Nov. 10, 1986. Throughout the past 35 years she served as a branch manager, opening the Crestview branch in July 1989 and the Bluewater Bay branch in May 1997. She was promoted to VP of Marketing/Compliance in January 2002 and was later promoted to SVP of Marketing/Compliance in May 2013. Cathie began her current role as chief strategy officer in October 2018. She oversees the coordination of the strategic plan and collaborates with the senior management team on project management. This past year Cathie spearheaded the yearlong Brand Refresh project with the Strum Agency.

"I would like to congratulate Cathie on her 35 years of service and thank her for her dedication to the employees and members of Eglin Federal Credit Union," said President and CEO Jerry Williams. "She makes decisions that are in the member's best interest while balancing compliance and risk considerations. In addition to her extraordinary experience, Cathie continues to shine with her positivity and enthusiasm to make Eglin Federal Credit Union the best it can be for members and employees."

Cathie states that she is grateful to love going to work each day, "I am privileged to work with a great team of dedicated professionals who are sincerely focused on our Mission."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

FORT WALTON BEACH, Fla. - Eglin Federal Credit Union is proud to once again support the United Way Emerald Coast's 28th Annual Day of Caring. Twenty-three employees painted and landscaped at the Emerald Coast Science Center in Fort Walton Beach and at the Crestview Manor in Crestview on Friday, Jan. 14. This year's Day of Caring aligned with Martin Luther King Day's National Day of Service celebrated on Monday, Jan. 17.

"In the words of Dr. Martin Luther King, Jr., life's most persistent and urgent question is: What are you doing for others?" said United Way Emerald Coast's President and CEO Kelly Jasen. "Eglin Federal Credit Union's employees continuously exemplify a spirit of giving back to the community, and we cannot thank them enough. Painting in the Emerald Coast Science Center and the Crestview Manor was extremely helpful to our local partners, saving them time and money. It's a wonderful way to give back, which ultimately benefits the people in Okaloosa County."

Eglin Federal Credit Union has sponsored and participated in this event for over 17 years, and employees have painted, cleaned, organized, gardened and more to help fill the needs of our community.

"This was a special day for a number of our employees to help the United Way Emerald Coast with projects around Okaloosa County at local non-profits," said VP Membership and Community Development Neko Stubblefield. "We look forward to the Day of Caring every year and hope our service at the Emerald Coast Science Center and Crestview Manor has made a positive impact. Giving back through service is one way to enhance our community!"

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

FORT WALTON BEACH, Fla. (Jan. 21, 2022) - Eglin Federal Credit Union is pleased to announce Mortgage Underwriter NormaJean Enlow has been selected as the 5-Star Performer of the 4th Quarter of 2021. NormaJean has been with the Credit Union for over 12 years and currently resides in Fort Walton Beach.

Along with President/CEO Jerry Williams, Mortgage Services Underwriting/QC Manager Mark Franks presented the award to NormaJean. He said, "NormaJean's work ethic and dedication are exceptional, and I do not use that adjective often. She always has a smile on her face, and she truly cares about our members as well as her fellow employees. She shows it in her willingness to help in any way, at any time every single day. Consistency is the word that comes to my mind. We are blessed to have her on our team."

The 5-Star Performer Award is a quarterly employee recognition program. The nominator provides a written submission describing how the employee exudes EFCU's Five Star Values: Respectful, Trustworthy, Dedicated, Proactive and Engaged.

Mortgage Services Operations Manager Ashley Hall and Mortgage Services Supervisor Christy Milian wrote the following in their nomination, "NormaJean Enlow is a 5-Star employee in every way. She is the ultimate team player in Mortgage Services and wears many hats in the department. There is no task too great for her to jump in (with a smile) and accomplish. NormaJean continually goes above and beyond what is expected of her. She radiates positivity and you cannot help but feel uplifted after even a short interaction with her. The Mortgage Services Department is lucky to have someone so committed to the job who is also a joy to be around. Congratulations, NormaJean, on an honor well-deserved!"

NormaJean was surprised and said, "Thank you for the nomination and award. It's a great honor, wonderful experience and a blessing to be given the opportunity to work with such professionals, wonderful staff and board who all have the best interest for our members."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

UPDATE August 23, 2022: Jonquil and Niceville Video Teller/ATMs are now open.

Fort Walton Beach, Fla. (Feb. 16, 2022) - Eglin Federal Credit Union is pleased to announce the ATM near Niceville High School and the ATM at the intersection of Jonquil Avenue NW and Mary Esther Cutoff NW in Fort Walton Beach are currently being upgraded to add more services with the installation of two drive-up Video Teller ITMs at each location. Construction is expected to be completed by the end of March for both locations. LaMacchia Group is the design/build firm for the project.

"Eglin Federal Credit Union continuously looks for ways to enhance the community in which we live and work," said CEO Jerry Williams. "Members will have two additional convenient locations where they can speak with a live Video Teller. At the same time, the community receives the benefit of an upgraded look at these sites in Okaloosa County."

Members will soon have the ability to speak with a live teller over two-way video between the hours of 9 a.m. and 5 p.m. Monday through Thursday and 9 a.m. and 7 p.m. Fridays at these locations.* Video Teller ITMs also operate as ATMs 24/7 using an EFCU ATM or Debit card. Additional drive-up Video Teller ITMs are located at most of our branches. In the meantime, members can view nearby surcharge-free ATMs at eglinfcu.org/locations/.

*Video Teller hours are not applicable on holidays.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Mar. 25, 2022) - Eglin Federal Credit Union is pleased to announce a new branch will be added in Freeport, Fla., making it the first location in Walton County. As part of the Credit Union's growth and expansion efforts, property was recently purchased at the intersection of Riverwalk Boulevard and US Highway 331, south of the Publix shopping center. Construction is expected to begin in a few months and be completed in 2023. La Macchia Group is the design/build firm for the new Freeport branch.

Eglin Federal Credit Union President/CEO Jerry Williams said, "We are looking forward to engaging with members at this new branch location in Freeport. This location was selected to add convenience for current members as well as to grow membership in Walton County. The members of this Credit Union are our neighbors, our communities, and we are proud to help them achieve their financial goals."

The new branch in Freeport will be approximately 4,000 square feet with two ITMs (Interactive Teller Machines) in the drive-up and additional ITMs in the foyer and lobby. The branch will have safe deposit boxes, Coinstar, night drop and a member engagement area with interactive touch screen monitors.

Last year Eglin Federal Credit Union added specific geographic locations in northern and central Walton County to its field of membership. Eligibility extends to persons who live, work (or regularly conducts business in), worship, or attend school in, and businesses and other legal entities located within the approved census tracts in Walton County. Learn how you are Eligible to Become an EFCU Member (eglinfcu.org).

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Apr. 21, 2022) - Eglin Federal Credit Union is pleased to announce a new branch will be added in Pace, Fla., making it the second location in Santa Rosa County. As part of the Credit Union's growth and expansion efforts, property was recently purchased at 4413 US-90 in Pace. Construction is expected to begin in a few months and be completed in 2023. La Macchia Group is the design/build firm for the new Pace branch, the Operations Center and the recently announced Freeport branch, all expected to be completed in 2023.

"We are excited to announce that the National Credit Union Administration has recently approved expanding our field of membership to include anyone who lives, works (or regularly conducts business in), worships or attends school, and businesses and other legal entities in specific geographic locations within Escambia County, Alabama as well as Escambia and Santa Rosa Counties, Florida," Eglin Federal Credit Union President/CEO Jerry Williams said. "The new branch location in Pace was selected to add convenient and affordable products and services as well as financial wellness resources to a growing membership. We will look for opportunities to partner with local chambers and businesses to add value to their community and employees. We do more than build credit. We build community."

The new branch in Pace will be very similar to the Freeport branch design with approximately 4,000 square feet, two ITMs (Interactive Teller Machines) in the drive-up and additional ITMs in the entry foyer and lobby. The branch will have safe deposit boxes, Coinstar, night drop and a member engagement area with interactive touch screen monitors.

Learn how you are Eligible to Become an EFCU Member (eglinfcu.org).

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Eglin Federal Credit Union is pleased to announce Supply Coordinator Kyle Tretter has been selected as the 5-Star Performer of the 1st Quarter of 2022. Kyle has been employed with the Credit Union since December 2020 and currently resides in Crestview.

President/CEO Jerry Williams and Facilities Manager/Security Officer Alan Campbell presented the award to Kyle. Jerry said, "Kyle's dedication to EFCU is evident in his performance. He is quick and responsive and goes over and beyond when things are requested from him."

Alan added, "Kyle is proactive in getting not only his job accomplished, but that of the mailroom without being asked to do so. He is always early to work and continually assists with extra duties. He is respectful to everyone he engages with and provides a helping hand to other departments when he sees their need. Kyle can be trusted and counted on to get the job accomplished, and done correctly."

The 5-Star Performer Award is a quarterly employee recognition program. The nominator provides a written submission describing how the employee exudes EFCU's Five-Star Values: Respectful, Trustworthy, Dedicated, Proactive and Engaged.

"I was extremely surprised and honored to receive this award," said Kyle. "I really enjoy working hard and being part of the Eglin Federal Credit Union team."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (May 25, 2022) - Eglin Federal Credit Union is pleased to recognize Bluewater Bay Branch Manager Susan Coup for her 30 years of service.

During her celebration Susan said, "I love what I do and have enjoyed serving our members at EFCU for 30 years!"

Susan joined the credit union in 1992 as a Records Vault Assistant. She transferred to Member Services in 1993 before being promoted to Account Services, where she held numerous positions from 1995 to 2010. From 2010 to 2013 she served as Records Vault Supervisor before being promoted to the Call Center Operations Manager from 2013 to 2020. In 2020, she transferred to our Bluewater Bay branch and is currently the Branch Manager. Susan earned a BS degree in Business Administration and attended the Leadership Okaloosa Class of 2006.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (June 27, 2022) - Eglin Federal Credit Union is pleased to recognize Senior Accountant Mark Sheltra for his 30 years of service.

"We'd like to thank Mark for his dedication and commitment to Eglin Federal Credit Union," said President/CEO Jerry Williams. "We appreciate his contributions throughout the years, which have helped us succeed and achieve our Mission."

During his celebration Mark said, "Thank you very much for this recognition. I am very proud to have served the members and employees of Eglin Federal Credit Union for 30 years. I am most proud of playing an integral role in the Y2K conversion."

Mark joined the credit union in 1992 as a Staff Accountant progressing to Senior Accountant in 2022. He earned a Bachelor of Science degree in Accounting with a minor in Computer Science from Western New Mexico University and a Master of Public Administration from Troy State University.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (June 28, 2022) - Eglin Federal Credit Union was recognized by the League of Southeastern Credit Unions and Affiliates as Credit Union of the Year in Florida for 2021 in the category of more than $500 million in assets. LSCU & Affiliates selected Eglin FCU for our outstanding service to members and the communities we serve. The award ceremony took place at the 2022 Southeastern Credit Union Conference and Expo in Orlando on Thursday, June 16. Read the LSCU news release here. Watch the announcement here.

"Eglin Federal Credit Union is very proud of being named the large Credit Union of the Year in Florida," said CEO and President Jerry Williams. "We are committed to making a positive difference in the lives of members and in our communities, and it feels great to be recognized for our accomplishments from 2021."

Some of the Credit Union's most recent impactful giving projects were helping launch an Okaloosa County Schools suicide-prevention program with the Hope Squad as a title sponsor, and EFCU is working closely to expand financial literacy in the classroom. EFCU partnered with the City of Crestview towards building the Eglin Federal Credit Union Skatepark benefitting area youth with the goal of reducing teen suicide. Watch the Skatepark video here.

"These projects came to fruition through proactive networking with community leaders," added Williams. "We live out the credit union philosophy of People Helping People."

Eglin Federal Credit Union continues to work closely with the United Way to give back during their Annual Day of Caring. EFCU has sponsored and participated in this event for over 17 years. Employees have painted, cleaned, organized, gardened and more to help fill the needs of our community. EFCU also partnered with the Boys and Girls Club of the Emerald Coast and Hey Gym Friend to conduct a Financial Fitness Bootcamp for approximately 100 youth on Friday, Nov. 5 at Riverside Elementary School in Crestview.

EFCU was also proud to be named the Large Business of the Year by the Crestview Area Chamber of Commerce, and the Credit Union was awarded the Corporate Business of the Year by the Fort Walton Beach Chamber of Commerce.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (July 6, 2022) - Eglin Federal Credit Union held a groundbreaking ceremony today at its new Pace Branch location. This will be the second Eglin FCU branch located in Santa Rosa County. The Navarre Branch opened nearly 15 years ago. As part of the Credit Union's growth and expansion efforts, property was recently purchased at 4413 US-90 in Pace. La Macchia Group is the design/build firm for the new Pace branch, the Operations Center and the recently announced Freeport branch, all expected to be completed in 2023.

"On behalf of the Eglin Federal Credit Union Board of Directors, I'd like to be one of the first to congratulate EFCU on this new location. As a local, I am excited we will be offering the benefits of membership to the Pace community and beyond," said EFCU Chairman William "Bill" Rone. "I am also a proud 50-year EFCU member who can tell the story of how there are more than 122,000 members worldwide, assets are approaching $3 billion, there's no debt, and EFCU receives top grades on external audit and examination reports. Eglin Federal Credit Union was recently awarded Credit Union of the Year for the State of Florida in the $500 Million and above asset size by the League of Southeastern Credit Unions. I believe TEAM EFCU epitomizes our motto, Where Members Matter Most."

The National Credit Union Administration recently approved expanding EFCU's field of membership to include anyone who lives, works (or regularly conducts business in), worships or attends school, and businesses and other legal entities in specific geographic locations within Santa Rosa and Escambia Counties, Florida and Escambia County, Alabama.

Eglin Federal Credit Union President/CEO Jerry Williams said, "We chose this location in Pace to provide convenient access to affordable products and services as well as financial wellness resources to our current members. There are approximately 1,500 members along the Highway 90 corridor in Santa Rosa County, and we are excited to extend the benefits of membership to our new neighbors as well as add value to this community."

The Pace branch will be approximately 4,000 square feet and will showcase a new open branch design that features universal employees, a member engagement area with interactive touch screen monitors. This will be a full-service branch with safe deposit boxes, coin counter, night drop, touch screen video tellers and drive up ATMs.

Media may contact Laura Coale for video b-roll and audio.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

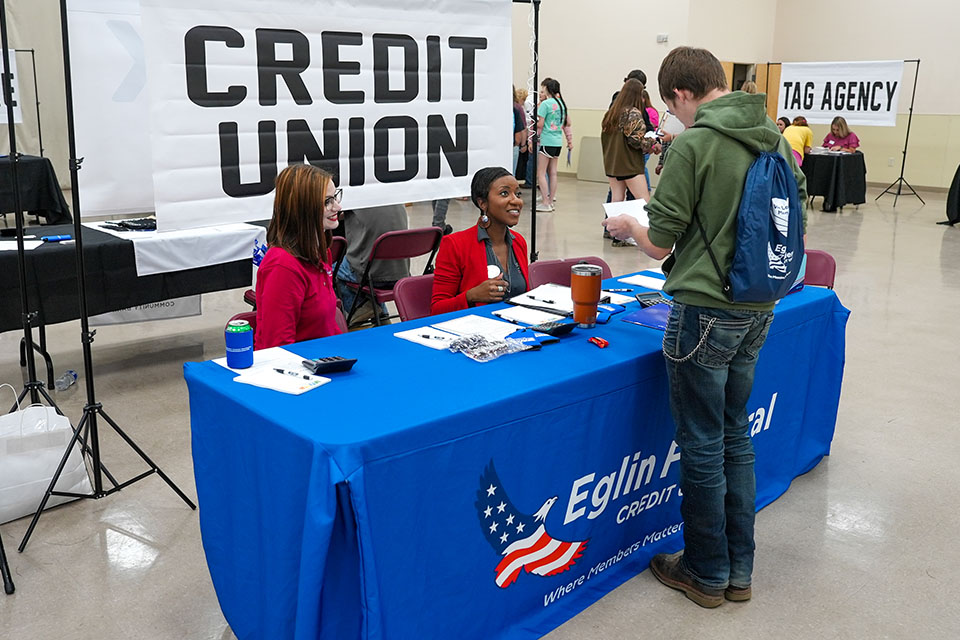

Fort Walton Beach, Fla. (July 20, 2022) - Eglin Federal Credit Union partnered with Okaloosa Saves for the annual Teach a Child to Save campaign April 1 - June 30. Youth were encouraged to set a savings goal and make a deposit into a savings account at EFCU. This year there were 90 youth under the age of 18 who participated with deposits totaling $18,685. Their names were entered into a random drawing for six children to win a $50 deposit into their EFCU account from Okaloosa Saves. Since the program began in 2004, there have been 2,172 children making deposits totaling $350,104.07.

The six winners were:

Genesis Albright, Fort Walton Beach

Dorothy Kollar, Fort Walton Beach

Mason Mueller, Fort Walton Beach

Nathan Smith, Crestview

Ruby Smith, Mary Esther

Soulina Sellers, Destin

The six winners were presented a certificate by Okaloosa Saves at the Okaloosa Board of County Commissioners board meeting on Tuesday, July 19. Chairman Mel Ponder, District 5, said, "Wise money management is such a beneficial skill to learn. The knowledge our youth gain in the Teach a Child to Save program will positively impact them now, their future families and businesses right here in our community in the years to come."

Eglin Federal Credit Union President/CEO Jerry Williams said, "Okaloosa Saves has been active in encouraging people of all ages to save money for life events. We are proud to have partnered with Okaloosa Saves for 18 years to help teach children the importance of saving, and we look forward to this program every summer."

Sherry Harlow, APR, serves on the Okaloosa Saves Board as the Treasurer and donated $1,000 to help with the Teach a Child to Save campaign. Harlow said, "It is never too soon to start teaching children to save. Helping them to develop good saving and spending habits in their youth can carry over into adulthood, especially in having funds for emergencies."

Savings Tips for Parents:

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (Aug. 9, 2022) - Eglin Federal Credit Union's Chairman of the Board of Directors William "Bill" Rone was inducted into the Defense Credit Union Council's Hall of Honor at their annual conference held in San Antonio, Texas on Aug. 4, 2022. The Defense Credit Union is a trade association representing more than 180 nonprofit defense credit unions with over 30 million members and $400 billion in assets. Bill is one of three honorees who were selected from a very competitive field of nominees by the Hall of Honor Selection Committee. They were selected for their impressive history of service and dedication to their military and veteran communities and are part of a history of excellence that exemplifies what it means to be a defense credit union. Read the DCUC announcement here and the conference wrap-up here.

"I am very proud to be inducted into the Defense Credit Union Council's Hall of Honor," said EFCU Chairman of the Board of Directors William "Bill" Rone. "As a 50-year member of Eglin Federal Credit Union and a member of the Board of Directors since 1979, I believe EFCU epitomizes our motto, Where Members Matter Most. It's been my pleasure to serve the members and employees of Eglin Federal Credit Union."

William "Bill" Rone has served on the Eglin FCU Board of Directors for 38 years using his experience of over 42 years in DOD federal service to improve the lives of members. Bill advanced from a GS-04 civilian cooperative education trainee on Eglin AFB to a member of the DOD Senior Executive Service as Senior Civilian and Comptroller for Air Force Special Operations Command. He was recognized with Presidential Meritorious Rank the first year he was eligible for the honor. His career took him to Washington DC for a one-year senior military school, four years on Robin AFB and two years with Naval Aviation Depot in Pensacola.

An expert in all areas of financial management with base credit union and bank liaison experience, he served and supported hundreds of thousands of active-duty, reserve, Air National Guard, and civilian professionals throughout his career. Rone has attended many DCUC conferences, including in an official capacity where he presented the Air Force Credit Union of the Year Award and led the Air Force breakout sessions. He has also served as both President and Vice President of chapters of the American Society of Military Comptrollers and is a lifetime member. Bill is a member of the University of West Florida Foundation Board of Directors and a Director Emeritus of the Special Operations Warrior Foundation where he served over a decade as Treasurer. He is also the Executive Financial Advisor for the Air Commando Association and a Trustee for their Foundation. As a member of the Santa Rosa Creek Indian tribe he volunteers as Financial Advisor to the Tribal Council and Chief.

"I'd like to thank Bill for the 38 years he has served on our Board, including eight years as Chairman and seven years as Vice Chairman," said EFCU CEO and President Jerry Williams. "We appreciate his commitment to our local community and our Credit Union. Bill's laser focus on meeting the needs of the Air Force to accomplish the mission, and developing people in his 'day job' was equaled by his dedication to the credit union movement. He is always ready to lead or assist as needed, making him a perfect fit for the DCUC Hall of Honor Award."

The DCUC Hall of Honor was established in 2000 as a means of recognizing those individuals whose exceptional contributions over the years have made a significant difference to DCUC and the defense credit union community. This prestigious award highlights the outstanding accomplishments of leaders, volunteers, management, and staff alike, whose efforts and endless support of the credit union movement and DCUC epitomize the Council's values and philosophy of "Serving Those Who Serve Our Country."

"These three honorees represent what the DCUC is all about, serving our military and veteran communities and providing extraordinary financial services that help them build their financial wellness. I'm in awe of their great leadership and am proud to honor their accomplishments," said Anthony Hernandez, DCUC President/CEO.

EFCU was recently named Florida's Credit Union of the Year by the League of Southeastern Credit Union and Affiliates. EFCU was also proud to be named the Large Business of the Year by the Crestview Area Chamber of Commerce, and the Credit Union was awarded the Corporate Business of the Year by the Fort Walton Beach Chamber of Commerce.

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (August 3, 2022) - Eglin Federal Credit Union is pleased to announce it will start developing a property located at 677 Highway 90 in DeFuniak Springs. The short-term plan is to install two drive-through ATM/Video Tellers. This will look similar to the drive-throughs currently being constructed near Niceville High School as well as the site at Jonquil Avenue NW and Mary Esther Cutoff NW in Fort Walton Beach. Construction of a full-service branch in DeFuniak Springs is expected to begin in late 2023 or early 2024. La Macchia Group is the design/build firm for the recently-announced Freeport Branch, the new Pace Branch, and the Operations Center.

"Our Field of Membership is growing and so are our branch locations," Eglin Federal Credit Union President/CEO Jerry Williams said. "The Credit Union is expanding our footprint to serve our current members closer to home as well as to provide convenient and affordable products and services, and financial wellness to a growing membership."

Members will have the ability to speak with a live teller over two-way video during our regular business hours. Video Teller ITMs also operate as ATMs 24/7 using an EFCU ATM or Debit card. Additional drive-up Video Teller ITMs are located at most of our branches. Find other nearby surcharge-free ATMs at eglinfcu.org/locations/.

Membership is open to those who live, work, worship, attend school and volunteer in seven geographic locations in Walton County. Learn how you are Eligible to Become an EFCU Member (eglinfcu.org/join/).

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (August 15, 2022) - Eglin Federal Credit Union is pleased to announce it will start developing a property located on the corner of Tiger Lake Drive and Highway 98 in Gulf Breeze. The short-term plan is to install two drive-thru ATM/Video Tellers in 2023. This will look similar to the drive-thrus currently being constructed near Niceville High School as well as the site at Jonquil Avenue NW and Mary Esther Cutoff NW in Fort Walton Beach, and the recently-announced location in DeFuniak Springs. Construction of a full-service branch in Gulf Breeze is expected to begin in 2024. La Macchia Group is the design/build firm for the Gulf Breeze and DeFuniak Springs locations as well as the upcoming Freeport Branch, the upcoming Pace Branch, and the Operations Center.

"The Credit Union is expanding our footprint to provide convenient and affordable products and services, and financial wellness to a growing membership," Eglin Federal Credit Union President/CEO Jerry Williams said. "We opened the Navarre Branch in 2007, the Pace Branch is under construction, and we are looking forward to adding Gulf Breeze as a third location in Santa Rosa County for members."

Members will have the ability to speak with a live teller over two-way video during our regular business hours. Video Teller ITMs also operate as ATMs 24/7 using an EFCU ATM or Debit card. Additional drive-thru Video Teller ITMs are located at most of our branches. Find other nearby surcharge-free ATMs at eglinfcu.org/locations/.

VP Membership and Community Development Neko Stubblefield added, "Membership is now open to those who live, work, worship, attend school and volunteer in specific geographic locations within Santa Rosa and Escambia Counties, Florida and Escambia County, Alabama. We look forward to continuing our relationship with Santa Rosa County residents and businesses as well as forming partnerships with nearby communities."

Follow Eglin FCU on Facebook, Instagram, YouTube and LinkedIn or visit our news and financial education page for updates. If you are interested in working at Eglin FCU, check out Careers at Eglin FCU.

###

Eglin Federal Credit Union was chartered in 1954 and is a not-for-profit, member-owned financial institution, federally regulated by the National Credit Union Administration. Membership includes military (active, retired, reserves and veterans), civil service and US Government affiliations on Eglin Air Force Base, Hurlburt Field, Duke Field, Camp Rudder and 7th Special Forces Group. Membership includes anyone who lives, works, worships or attends school within our Geographic Field of Membership and anyone who is related to or lives with an Eglin FCU member. Membership also includes over 900 Select Employee Groups in Okaloosa, Santa Rosa, Walton, Escambia, FL counties and Escambia County, AL.

Our Mission is to provide our members with five-star service, support and solutions to simplify their financial lives.

Where Members Matter Most.

Fort Walton Beach, Fla. (August 30, 2022) - Eglin Federal Credit Union held a groundbreaking ceremony today at its new Freeport Branch, making it EFCU’s first location in Walton County. As part of the Credit Union’s growth and expansion efforts, property was recently purchased at intersection of Riverwalk Boulevard and US Highway 331, south of the Publix shopping center in Freeport. La Macchia Group is the design/build firm for the new Freeport Branch, the upcoming Pace Branch, the Operations Center and the recently-announced DeFuniak Springs and Gulf Breeze locations.

"On behalf of the Eglin Federal Credit Union Board of Directors, we are very proud to start on the construction for our first branch in Walton County,” said EFCU Chairman William “Bill” Rone. “I am excited we will be offering our current members this convenient location and also to extend the benefits of membership to the Freeport community.”

Last year Eglin Federal Credit Union added specific geographic locations in northern and central Walton County to its field of membership. Eligibility extends to persons who live, work (or regularly conducts business in), worship, or attend school in, and businesses and other legal entities located within the approved seven census tracts in Walton County. Learn how you are eligible to become an EFCU member..